On a global scale, the energy transition has accelerated significantly in the economic context of recent years, although its evolution in the coming years remains uncertain. As evidence, the size of the global market for the six main mass-produced low-carbon technologies – solar photovoltaic, wind power, electric vehicles, batteries, electrolyzers and heat pumps – has almost quadrupled between 2015 and 2023, reaching more than 700 billion dollars, or approximately half the value of all natural gas produced globally. This growth has been driven by massive deployment of clean technologies, particularly for electric vehicles, solar photovoltaic and wind power. With the policies announced for the coming years, the market for these low-carbon technologies could triple by 2035 to exceed 2,000 billion dollars, roughly the size of the global crude oil market today.

The IEA recently published its report "Energy and Technology Perspectives 2024" (ETP-24) in which it notably highlights existing opportunities that could make emerging economies important players in the manufacturing of new low-carbon technologies and their commercial exchanges. Through the collection of country-by-country data on more than 60 indicators, assessing the business environment, energy and transport infrastructures, resource availability and domestic market size, the IEA notably identified North African countries and particularly Morocco as potential important players within its scenarios analyzing the industrial sectors of electric vehicles and their batteries.

Jules Sery, consultant at the IEA and co-author of the report, presents us with the main elements.

Interview conducted by Karim Lasri

KL: Morocco has many assets, positioning it as a high-potential player in the supply of electric vehicles and batteries. What are the existing infrastructures that place it as a key link in this industry?

In total, the country currently benefits from an annual production capacity of 650,000 vehicles, mainly from the factories of European manufacturers such as Renault and Stellantis, whose investments have considerably boosted the sector in the kingdom. They invested in the country to take advantage of reduced labor and energy costs.

We can also cite proximity to the considerable European market and robust transport infrastructure as favorable conditions for Morocco's emergence as a strategic industrial partner. The Tangier Med port, one of the largest in the Mediterranean, illustrates this infrastructure capable of facilitating rapid and efficient shipments, thus reducing logistics costs and delivery times.

KL: Beyond the infrastructures you mention, does Morocco have crucial primary resources for its economic potential in the electric vehicle and battery sectors?

JS: We often think of phosphate exploitation as Morocco's main mining activity, and to a lesser extent of cobalt. The country has the largest known reserves to date. This mineral is more widely known for its use in the manufacture of chemical fertilizers essential to modern agriculture than for its critical use in the manufacture of Li-ion batteries for electric vehicles. Indeed, today two particular technologies, or cathode chemistry, share the global Li-ion battery market: NMC batteries (Nickel, Manganese, Cobalt) preferred in Western markets and LFP (Lithium Iron Phosphate) batteries dominant in the Chinese market. Over the past 5 years, the rise of China's Li-ion battery industrial sector has increased the share of LFP technology in the global EV battery mix, doubling it between 2020 and 2023 to reach 40% of the global market. In industry parlance, this is referred to as the "LFPification" of the global lithium-ion battery market. The lower manufacturing cost of LFP batteries compared to their NMC counterparts suggests that this trend is likely to strengthen in the short and medium term, barring major technological disruption in the field.

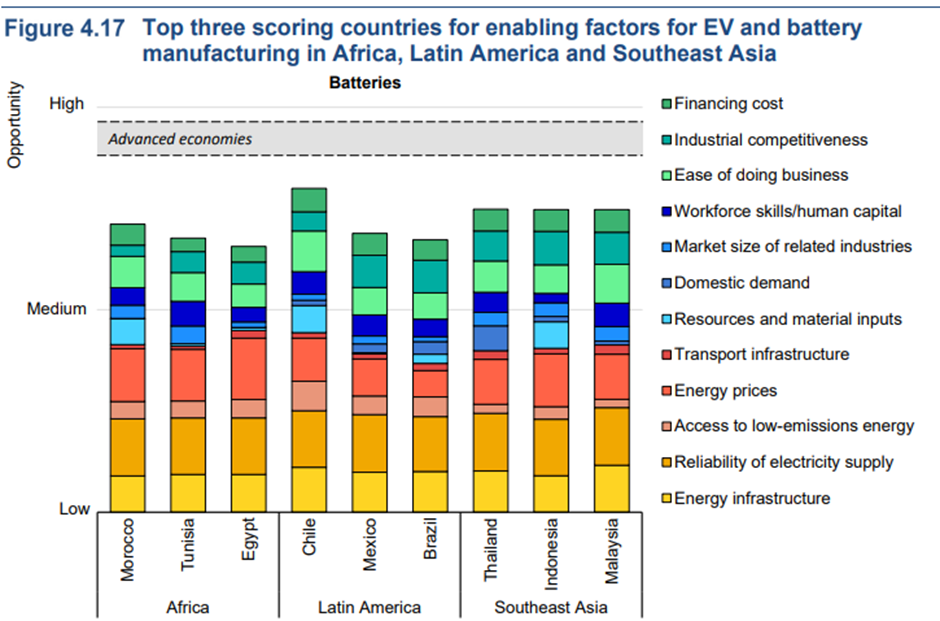

Above, the graph shows the potential main players for the manufacture of electric vehicles and batteries in Africa, Latin America and Southeast Asia. Morocco appears as a potential leader on the African continent, with Tunisia and Egypt. The respective contributions of multiple factors, ranging from energy infrastructures to industrial competitiveness to domestic demand, are notably represented.

In this context, Morocco has the potential to leverage its substantial phosphate resources to develop an LFP battery industrial sector where Europe has historically focused on NMC technology due to its higher energy density. Furthermore, the country has low-cost energy resources and easy access to low-carbon energy that can contribute to the emergence of such a sector (Africa's largest solar complex is located in Ouarzazate and has a capacity of 500 MW). The availability of a skilled workforce, at lower cost from the perspective of certain economies, is also an attractive factor for potential foreign investors wishing to take advantage of this range of resources.

KL: Because of these assets you mention, Morocco has already attracted Chinese investments for the production of electric vehicles and batteries. What is the content of the projects underway?

JS: Indeed, several foreign investors are interested in Morocco to establish an industrial battery sector in light of the advantages mentioned above. We can notably cite Chinese industrialists CNGR Advanced Material Company and Gotion, which have respectively announced investments of 2 and 6.5 billion dollars in the short term in the country. Gotion plans to build an industrial complex there around LFP technology capable of reaching an annual production of 100 GWh. To put this in perspective, if this project comes to fruition, its production capacity will exceed that of LG Energy Solution, currently the largest European battery factory in operation with 86 GWh of capacity. Other Asian industrialists, notably South Korean LG Chem and Chinese Youyshan, have also recently announced significant investments in the country. All these projects will allow Morocco's industrial battery sector to develop considerably to thus meet the strong demand created by electric vehicle sales in the main markets neighboring Morocco, Europe first and foremost.

KL: The global economy is marked by a massive increase in investments in clean energy: 50% increase in 2023. However, well-designed trade policies are considered essential for the transition to clean energy to continue to accelerate. In this context, could trade agreements favorable to Morocco attract new investments in these sectors from partners other than China?

JS: Morocco has signed important free trade agreements with its main trading partners, starting with the European Union in 1996 and the United States in 2004. These trade agreements notably allow Morocco to free itself from tariffs and quotas that could hinder the competitiveness of its exports. Moreover, the free trade agreement signed with the United States has a double advantage as it allows electric vehicles equipped with batteries manufactured in Morocco to be eligible for the tax credit granted under the American Inflation Reduction Act (IRA). All of these trade agreements offer Morocco's industrial electric vehicle and battery sector tremendous export opportunities that would allow domestic production to considerably exceed still nascent domestic demand that is too underdeveloped to enable a true industrial boom in these technologies.

KL: In view of all these elements, what projections can reasonably be made regarding the development of the electric vehicle sector in Morocco?

JS: As part of our ETP-24 report, we developed a model implementing all the favorable conditions for the emergence of an industrial electric vehicle and battery sector in Morocco in order to assess future trajectories of production and commercial exchanges of these technologies according to different scenarios.

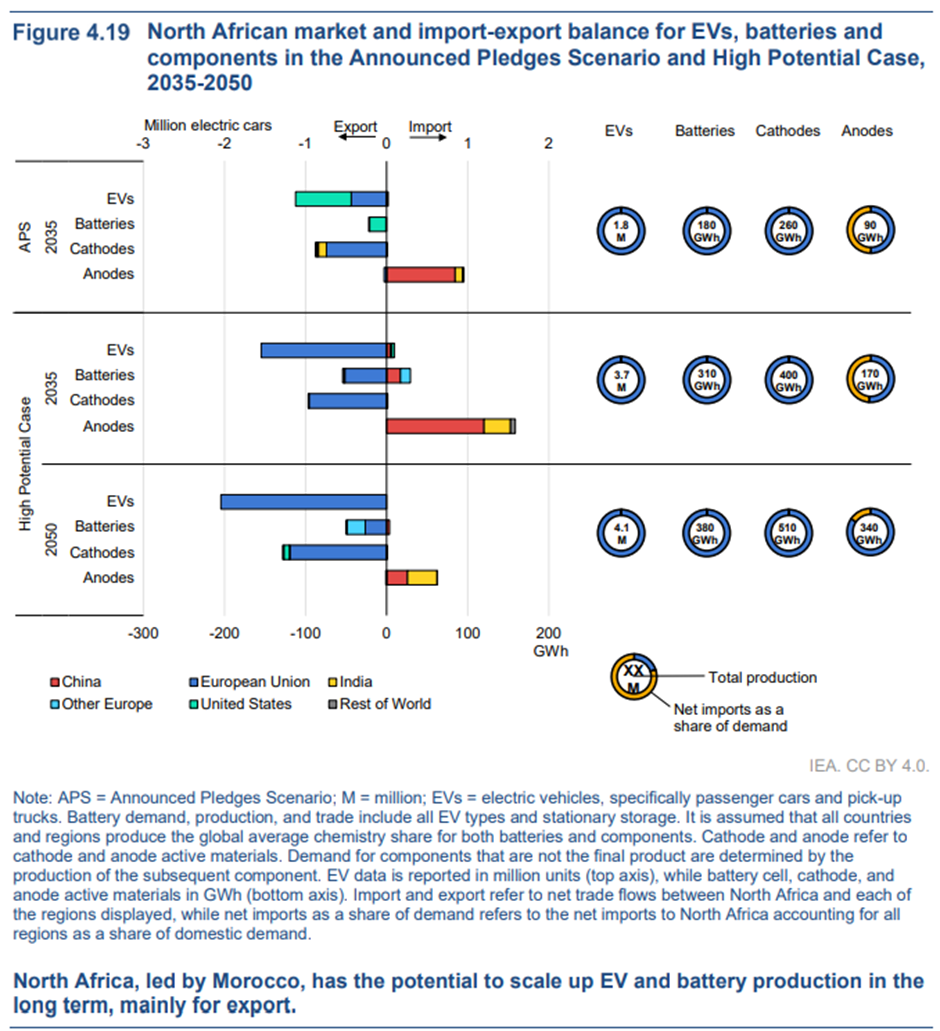

The graph above shows, among other things, the import-export balance of electric vehicles and batteries, in millions, for North African countries, and in two scenarios: that of the objectives already set by governments (APS), and a more optimistic scenario (High Potential Case) that assumes that the economies concerned exploit all their competitive advantages by overcoming many barriers to the development of these markets. It shows the potential for exports from North African countries, and explicitly mentions Morocco's leadership position due to its ability to scale up its production of electric vehicles and batteries.

The "Announced Pledges Scenario" (APS) examines what would happen if all national energy and climate objectives set by governments, including net-zero targets, were met on time and in their entirety. In this scenario, the IEA estimates that North Africa, with Morocco in the lead, will produce almost 1.8 million electric vehicles in 2035, of which 70% would be intended for export to the USA and the European Union. This production of electric vehicles will in turn generate a battery demand of almost 200 GWh entirely satisfied by local production. A second scenario called the "High Potential Case" (HPC) was developed to estimate the impact on global production and trade of these technologies of a demand for electric vehicles and batteries compatible with a net-zero CO2 emissions target in 2050. Within our HPC scenario, Morocco could see its production of electric vehicles and batteries reach more than 3.5 million and 300 GWh respectively by 2035. In 2050, in the HPC scenario, the development of Morocco's industrial sector as well as increased global demand for electric vehicles and batteries could increase domestic production to more than 4 million electric vehicles, of which more than half would be intended for exports to the European Union.

KL: To conclude, this recent IEA report highlights the considerable economic and strategic opportunities that the energy transition offers to countries like Morocco, which have many resources, solid industrial infrastructure and an advantageous geographic position. With a clear vision and appropriate policies, Morocco has the potential to become a major player in the manufacture of electric vehicles and batteries, thus helping to meet the growing demand for low-carbon technologies.

Foreign investments, free trade agreements and low-cost energy resources strengthen this outlook. By capitalizing on these assets, Morocco can not only diversify its economy, but also play a key role in integrating emerging economies into the global value chain of electric vehicles and batteries.

The scenarios developed by the IEA show that Morocco's future in this sector is promising, provided it continues to attract investments and adopt strategies favorable to the industrialization of the country and exports. This development could thus sustainably place the Kingdom in the dynamics of the global energy transition.

This interview was conducted by Karim Lasri

Link to the "Energy and Technology Perspectives 2024" report ETP-24